Global financial markets are showing cautious movement as investors anxiously await Federal Reserve Chair Jerome Powell's upcoming speech at the annual Jackson Hole economic symposium. The highly anticipated address comes amid ongoing debates about the Fed's monetary policy direction and its impact on various asset classes [1].

In a significant move affecting global metals trade, India has announced new protective import tariffs on steel products, citing a sharp increase in foreign imports threatening domestic producers. The measure, which will extend over three years, comes amid broader international trade tensions and represents one of the most substantial trade barriers recently erected in the Asian steel market [1].

Global fast fashion retailer Shein is demonstrating remarkable financial performance as it prepares for its highly anticipated initial public offering (IPO). The company has posted impressive growth figures in key markets, particularly in the United Kingdom, where it achieved a substantial profit increase and significant market expansion [1].

A dramatic shift is unfolding in cryptocurrency markets as major institutional players like Goldman Sachs, Brevan Howard, and Harvard have significantly increased their Bitcoin exposure through spot ETFs [1], while veteran trader Peter Brandt projects Bitcoin could reach $145,000 in the coming weeks [2]. However, this institutional optimism contrasts sharply with growing bearish sentiment among active crypto traders.

Recent economic data shows inflation maintaining a moderate pace, with the consumer price index holding at 2.7% year-over-year in July [1]. This figure, coming in slightly below market expectations, provides a mixed signal as the Federal Reserve contemplates its next moves on interest rates amid evolving economic conditions.

Global stock markets showed mixed performance as major indices retreated slightly from their recent record levels. The day's trading reflected ongoing tension between optimistic market sentiment and growing concerns about potential overvaluation, particularly in the artificial intelligence sector. While the Dow Jones Industrial Average managed to eke out a small gain, both the S&P 500 and Nasdaq finished lower [1].

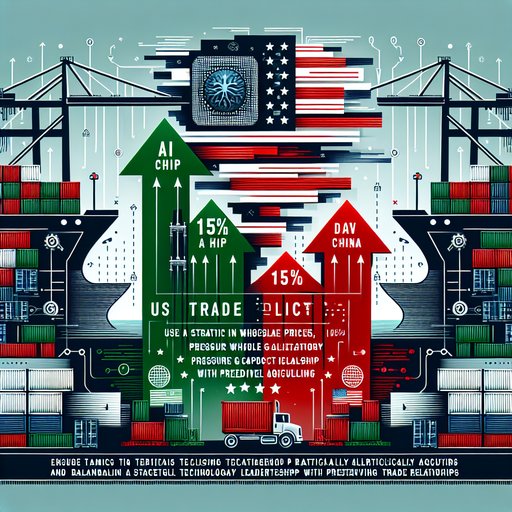

In a significant shift in tech trade policy, the US government has implemented a 15% tax on AI chip sales to China, affecting major manufacturers like NVIDIA and AMD. This move comes just weeks after lifting an earlier ban on NVIDIA's H20 AI chip sales, marking a new approach to maintaining American technological dominance while allowing controlled trade [1].

Financial markets are showing optimism as expectations grow for the Federal Reserve to cut interest rates in September, even as recent economic indicators present a mixed picture. The S&P 500 futures have edged higher [1], with investors largely shrugging off concerns about potential inflationary pressures highlighted by some Fed officials.

In a significant move that signals growing institutional interest in cryptocurrency, Bitcoin Standard Treasury Co. has announced plans to go public through a SPAC merger valued at $2.1 billion. The deal represents one of the largest cryptocurrency-focused public offerings this year, as the company positions itself to compete with established players in the Bitcoin mining and holdings sector [1].

Recent labor market data reveals contrasting trends across different sectors and regions, with the United States showing some positive indicators despite significant organizational restructuring in certain agencies. The Department of Labor reported a decrease in weekly unemployment claims to 224,000 [1], while simultaneously, major changes are underway at federal agencies and tech companies.